Table of Content

As an alternative to including this statement, creditors may provide an itemization of such fees with the early disclosures. Any itemization provided upon the consumer's request need not include a disclosure about property insurance. When you’re approved for a HELOC, you will also be approved for a credit limit based, in part, on how much equity you have in your home. You can use this line of credit during what is called the “draw period.” This is the amount of time you have to draw funds from the HELOC. The draw period typically lasts for a fixed amount of time. It can vary between lenders, but the period usually can last up to ten years.

If you find yourself in this predicament, see if your lender is open to some type of loan modification. Paying back at least some of the principal during the draw period reduces the total amount you will owe when the HELOC closes. If you pay it all back, you'll have a zero balance at the end of the draw period. In this case, your loan will close—generally with no further payments or action required on your part. The cost a customer pays to a lender for borrowing funds over a period of time expressed as a percentage rate of the loan amount.

Refinance the Balance Into Your Primary Mortgage

Make sure you can comfortably afford your increased payment on top of your regular monthly mortgage payment. Any additional principal payments made during the draw period on a HELOC will reduce the payments due during the HELOC's repayment period. During the draw period, your online account through your HELOC servicer should show you estimates of what your monthly payment will be during the repayment period. After the draw period of a HELOC is over, you enter the repayment period. At this point, the loan converts to a repayment schedule, during which both principal and interest will be due every month. Because you’re only charged for your outstanding balance at the end of your draw period, your monthly repayment amount will largely depend on how much you’ve borrowed.

One distinguishing feature of HELOCs is that they come with draw periods normally ranging from 5 to 10 years. Bankrate.com is an independent, advertising-supported publisher and comparison service. We are compensated in exchange for placement of sponsored products and, services, or by you clicking on certain links posted on our site. Therefore, this compensation may impact how, where and in what order products appear within listing categories.

How long does it take to get a home equity line of credit or home equity loan?

Ask for your credit score.Credit scoringis a system creditors use to help decide whether to give you credit. Keep in mind the risks involved when using your home as collateral. If you can’t pay the money back, you could lose your home to foreclosure.

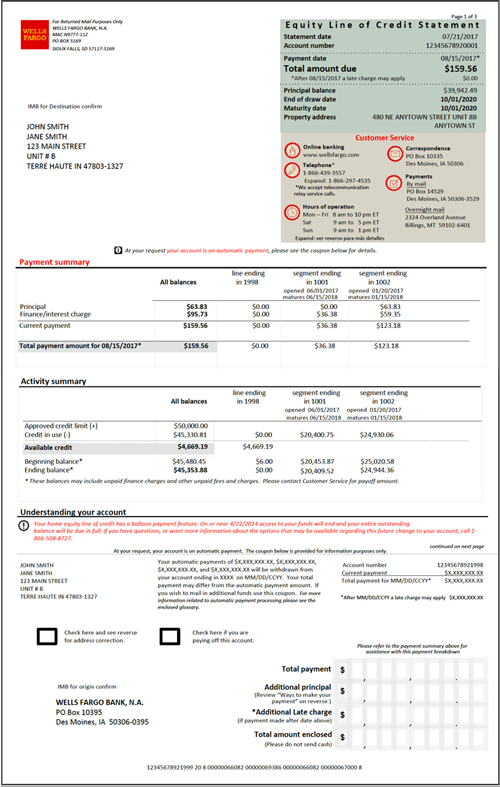

Use of this site constitutes acceptance of our Terms of Use, Privacy Policy and California Do Not Sell My Personal Information. NextAdvisor may receive compensation for some links to products and services on this website. “As a line of credit, you can use it repeatedly and make draws to meet your needs,” says Jon Giles, senior vice president and head of consumer direct lending at TD Bank. “Instead of borrowing everything on day one, you can withdraw funds as you need them,” he explains. A large lump-sum payment due at the end of some types of home equity lines of credit.

Can I change the interest rate on my home equity line of credit from a variable to a fixed rate?

Before you fill out your application, make sure you know the terms of a HELOC and understand it’s fundamental aspect—the draw period—to know if it’s right for you. The draw period length depends on your HELOC’s exact terms and conditions. Generally, the draw period lasts between five and ten years. After the draw period is over, you will no longer be able to withdraw any funds from your HELOC.

Usually that’s the first step inthe foreclosure process. Refinancing your home, getting a second mortgage, taking out a home equity loan, or getting a HELOC are common ways people use a home as collateral for home equity financing. But if you can’t repay the financing, you could lose your home and any equity you’ve built up.

What is the fixed rate option?

After several years of making interest-only payments, the jump to full interest and principal payments can come as a shock, so make sure you review your loan documents and make note of when your HELOC will enter repayment. “Be prepared to make that full payment when the loan converts to a fully amortized payment schedule,” says Tabitha Mazzara, director of operations with the Mortgage Bank of California . The draw period is the predetermined length of time you can use your revolving line of credit. During the draw period, you can withdraw from your HELOC account to pay for any expenses you may have. Made interest-only payments, the principal balance remains the same through the term of the account.

For example, if you get a $100,000 HELOC and only draw $20,000, you will only have to pay back the $20,000 plus interest, not the full $100,000 you could have drawn. When you need to cover a big expense, such as home remodeling, a child's wedding or an unexpected hospital bill, a home equity line of credit is one option for getting the cash you need. A home equity line of credit is a type of revolving credit that allows you to borrow against the equity in your home.

Then, you must offer to return the lender’s money or property. If the lender doesn’t claim the money or property within 20 days, you can keep it. And be sure to avoid any lender who promises one deal when you apply, but gives you a different set of terms to sign, with no good explanation of the change.

You can borrow up to the limit, pay it back and then borrow more money as many times as you want until the draw period comes to a close. The money from your HELOC can be used to pay off other higher-interest debt, make home improvements, remodel or almost any other purpose. You may encounter harmful practices related to the day-to-day management of your mortgage payments. There are several types of servicing abuses, including a lender charging you improper fees or not giving you accurate or complete account statements and payoff figures.

Take a close look at all your options and make sure you budget carefully. This will help ensure that you’re not caught off guard during your loan repayment process—no matter what type of loan you choose. Once your HELOC's draw period expires, you'll be unable to access any remaining approved loan amounts. Also, you're not obligated to draw the entire HELOC loan amount before the draw period expires.

Your personal credit report includes appropriate contact information including a website address, toll-free telephone number and mailing address. If that's not possible, you have several options for refinancing or closing your HELOC before the draw period ends. The length of time during which you can access funds from your account. Maximum lendable equity is the maximum amount available to borrow, typically up to 80% of a home’s value after subtracting any existing mortgage balance. © 2022 NextAdvisor, LLC A Red Ventures Company All Rights Reserved.

No comments:

Post a Comment